2026 Interest Rate Cuts: How Much Could You Really Save on Your Home Loan?

Explore the latest SARB repo rate updates and forecasts for 2026 interest rate cuts in South Africa, with real savings examples for home loans—including a personalised Durbanville scenario.

2026 Interest Rate Cuts: How Much Could You Really Save on Your Home Loan?

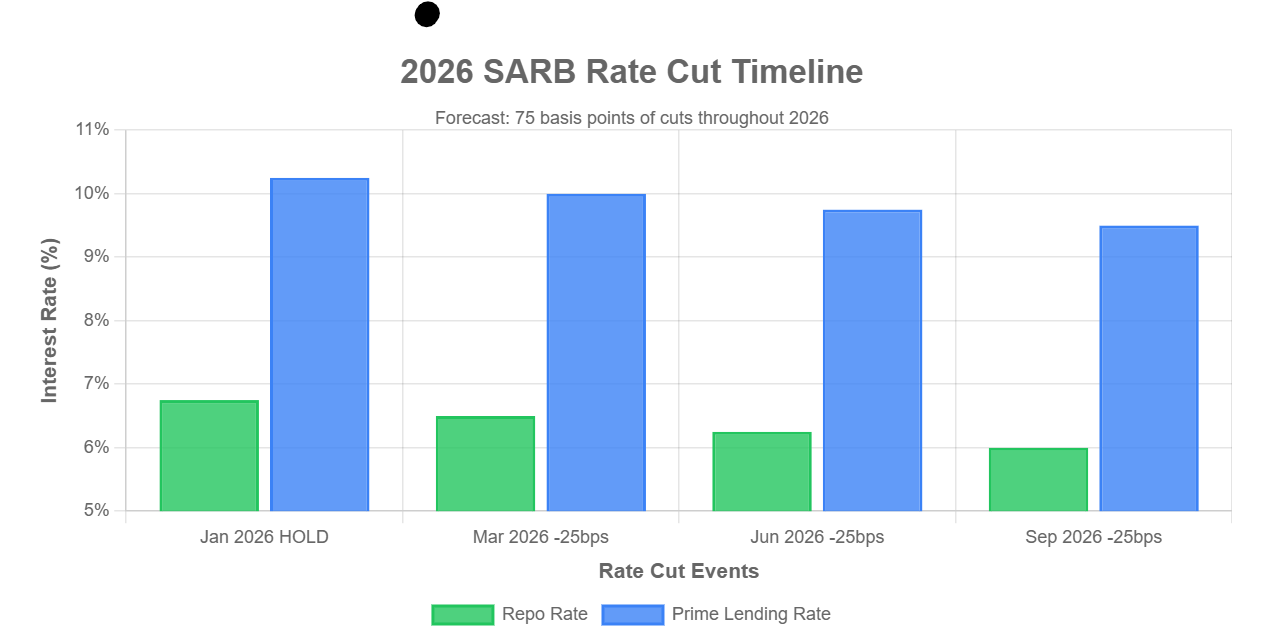

It's early January 2026, and South African homeowners are watching the SARB closely. The repo rate stands at 6.75% (prime lending rate 10.25%) after the unanimous 25 basis point cut in November 2025. Economists widely expect a pause at the upcoming January MPC meeting (29 January), but forecasts point to gradual cuts totalling 50–75 basis points throughout 2026 as inflation trends lower toward the new 3% target.

These cuts could translate into meaningful monthly savings on variable-rate home loans—potentially freeing up cash for emergency funds, debt reduction, or investments.

Current Rates and 2026 Outlook

As of January 2026:

- Repo rate: 6.75% (unchanged since November 2025)

- Prime lending rate: 10.25%

Inflation is projected to average around 3.5–3.6% in 2026, giving the SARB room for easing.

Most analysts predict:

- A hold in January

- 25bps cuts starting March or later

- Total 50–75bps reduction by year-end

Every 25bps cut typically reduces repayments by ~R168 per R1 million borrowed (20-year term).

Projected rate cuts: January hold at 6.75%, then three 25bps cuts throughout 2026 bringing repo rate to 6.00%

Projected rate cuts: January hold at 6.75%, then three 25bps cuts throughout 2026 bringing repo rate to 6.00%

Sources: SARB statements, BusinessTech (December 2025), Trading Economics forecasts.

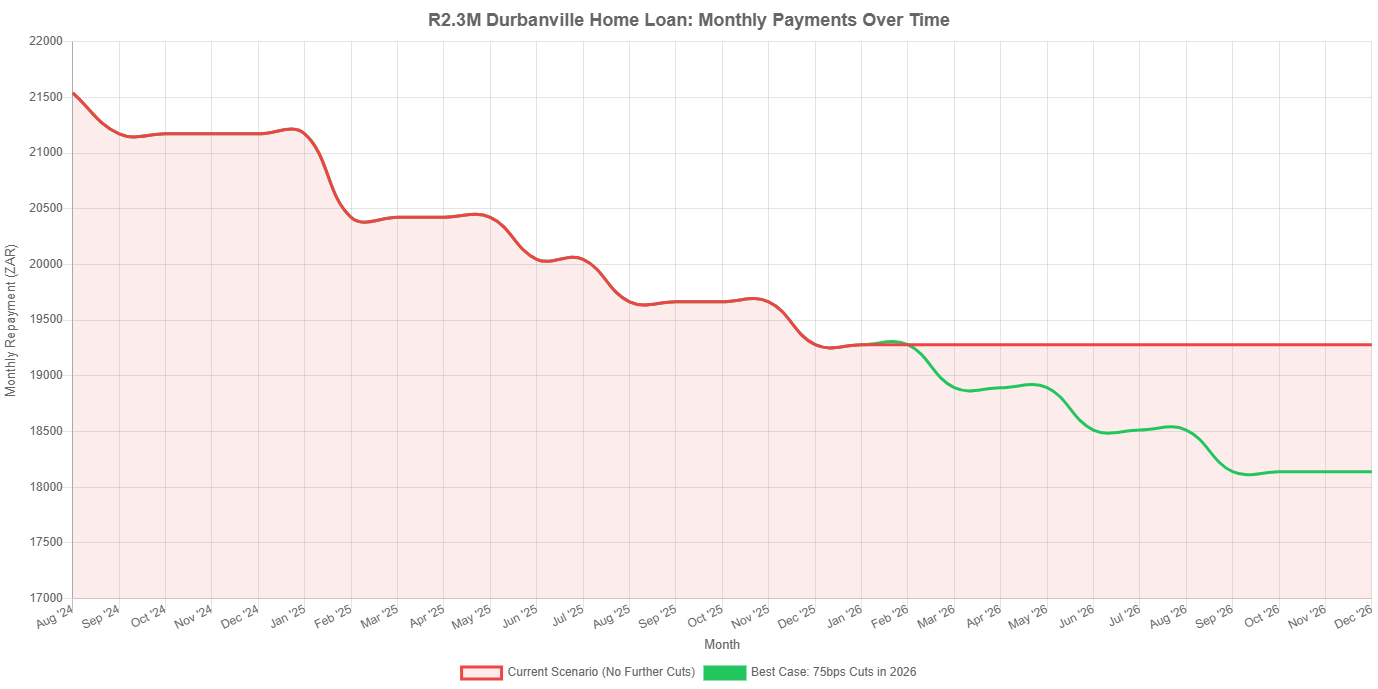

Real-Life Example: A R2.3 Million Durbanville Home Loan

Let's make this personal. Consider a Western Cape bank employee who purchased a beautiful 3-bedroom house in Durbanville for R2.3 million in 2024:

- Full bond (no deposit; transfer fees paid separately)

- 20-year term starting August 2024

- Favourable rate: prime minus 2.5% (staff benefit)

- No extra payments

Current effective rate (January 2026): 10.25% – 2.5% = 7.75% Current monthly repayment: Approximately R19,280

Savings Scenarios for 2026

Here's a projected repayment timetable based on economist consensus for 2026 cuts (savings compound over the remaining term):

| Scenario | Your Effective Rate | Monthly Repayment | Monthly Saving vs Current | Potential Annual Saving |

|---|---|---|---|---|

| Current (no further cuts) | 7.75% | R19,280 | - | - |

| After 25bps cut (e.g., March) | 7.50% | R18,894 | R386 | R4,632 |

| After 50bps cumulative | 7.25% | R18,514 | R766 | R9,192 |

| After 75bps total (end-2026) | 7.00% | R18,140 | R1,140 | R13,680 |

Calculations use standard amortising bond formula. Actual savings may vary slightly as banks recalculate on remaining balance. Over the full remaining term (~18.5 years), 75bps could save over R200,000 in interest.

Payment Trend Over Time

The chart below visualizes how your monthly payments have already evolved since August 2024 (starting at R21,540), and projects future savings with anticipated rate cuts through 2026:

The green line shows the best-case scenario with full 75bps cuts by end of 2026, saving you R1,140 per month compared to current rates.

The green line shows the best-case scenario with full 75bps cuts by end of 2026, saving you R1,140 per month compared to current rates.

Savings for Average South African Home Loans

For context, here's what 75bps of cuts could mean for different loan sizes:

- R1.5 million bond: ~R750/month saving (R9,000/year)

- R2 million bond: ~R990/month saving (R11,880/year)

- R3 million bond: ~R1,485/month saving (R17,820/year)

These reductions add up quickly, especially when redirected wisely. Imagine what you could do with an extra R13,680 per year from the Durbanville example above. Use our Bond Affordability Calculator to calculate your own bond savings scenarios.

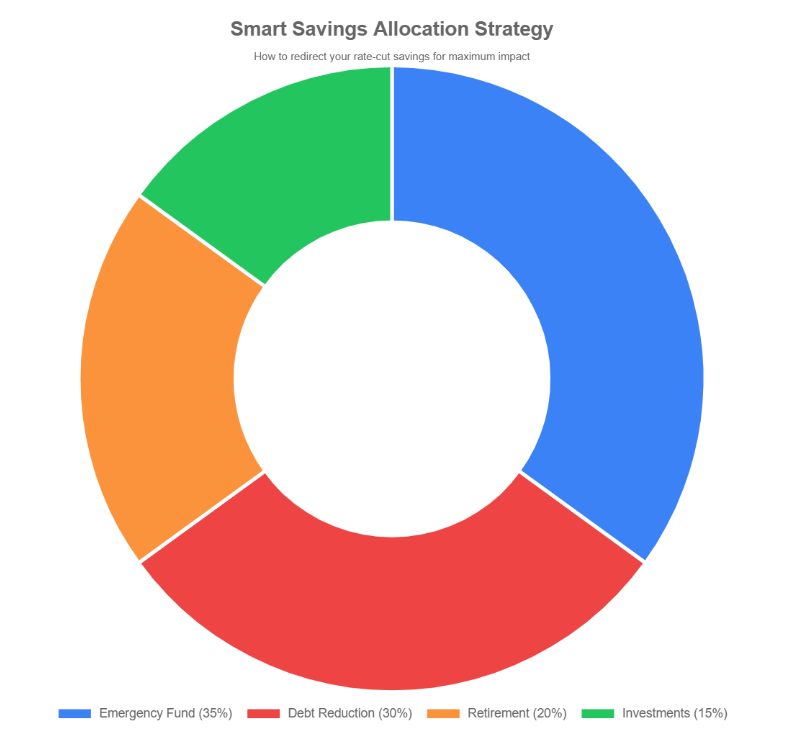

What to Do with Your Potential Savings

Lower bond repayments create breathing room in your budget. Here is a smart breakdown of how you can redirect those savings for maximum financial impact:

Recommended allocation: Prioritize emergency fund (35%) and debt reduction (30%), followed by retirement (20%) and investments (15%)

Recommended allocation: Prioritize emergency fund (35%) and debt reduction (30%), followed by retirement (20%) and investments (15%)

Priority 1: Build Your Safety Net

- Emergency fund (aim for 3–6 months' expenses) - Calculate your target with our Emergency Fund Calculator

- Start with R500-1,000/month if you're beginning from zero

Priority 2: Eliminate High-Interest Debt

- Credit cards (18-24% interest)

- Personal loans and store accounts

- Snowball method: smallest balance first for psychological wins - Compare strategies with our Debt Payoff Calculator

Priority 3: Secure Your Future

- Increase retirement contributions (tax-deductible!)

- Even R500/month compounds to significant amounts over 20 years

Priority 4: Spot Budget Leaks

- Review subscriptions you're not using

- Entertainment overspending

- Use MyFinHealth to identify patterns automatically

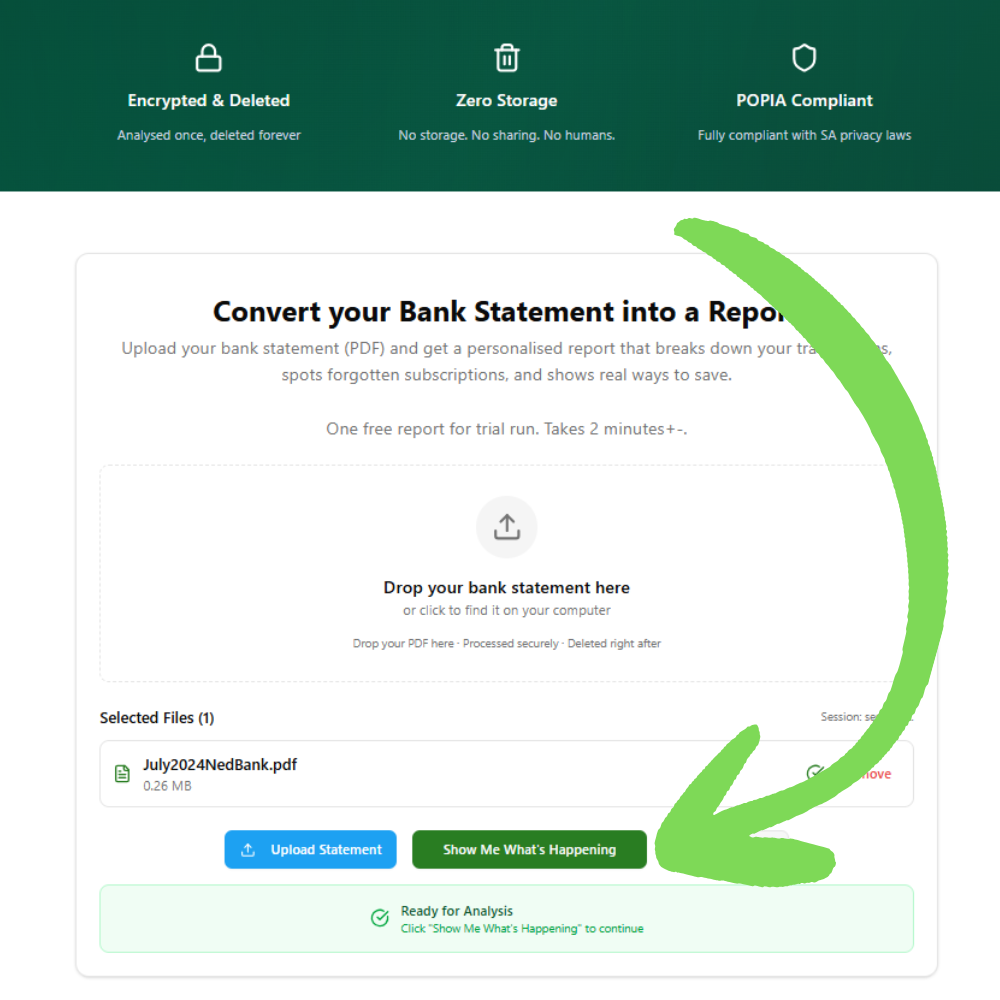

Don't Just Hope for Savings—Track Them in Real-Time

Rate cuts only help if you actually redirect those savings instead of letting them disappear into everyday spending. That's where MyFinHealth comes in.

MyFinHealth is the secure, POPIA-compliant platform built for South Africans to get clear financial insights from bank statement PDFs.

Simply upload your statements and instantly see:

- Your exact home loan debit order highlighted and categorised

- Personalised financial health score factoring in debt ratios

- Spending trends and overspending alerts

- Actionable tips: "Redirect rate-cut savings here to boost your score"

Users often discover hidden fees draining potential savings—before rate cuts even arrive. Visit MyFinHealth Pricing to get started with your first analysis.

Sources: South African Reserve Bank (resbank.co.za), BusinessTech (Dec 2025–Jan 2026 articles), Trading Economics, ooba Home Loans bond calculator data.

Have questions? Contact us at support@myfinhealth.com – we're here to help!

Written by

Steven

Founder, MyFinHealth